Alternatives

New opportunities in private credit, powered by BMO GAM

September 20, 2024

Even as financial markets experience heightened volatility and uncertainty, opportunities for private credit are expanding. Globally, private lending is expected to more than double by 2028, to US$3.5 trillion compared to US$1.7 trillion today.1 Current rates have made private lending appealing, with its more flexible terms and floating rate structures that can generate attractive risk-adjusted returns.

In Canada, as capital requirements for conventional financial institutions become more onerous, opportunities are opening up to develop new models and fund structures within private credit, including sub-asset classes such as commercial real estate and private equity-sponsored financing.

These developments mean that higher quality borrowers that may otherwise have issued debt in the public markets are seeking alternative avenues, attracted by financing certainty and efficient completion of transactions among other factors. For investors, such loans are priced at wider spreads relative to similar-maturity high-yield bonds or leveraged loans, and offer higher overall yields while still adhering to more conservative capital structures.

In both the near and long term, private credit is a growth centre in Canadian capital markets, creating a unique opportunity to develop a robust pipeline of innovative investment vehicles that are accessible to a growing number of accredited investors.2

Resilience of private credit

We tend to think about the resilience of private credit over the long term, and how the asset class has performed over cycles. These are floating rate assets, meaning their return is based on a floating rate benchmark. The spread over the benchmark is meant to reflect the credit risk of the underlying asset.

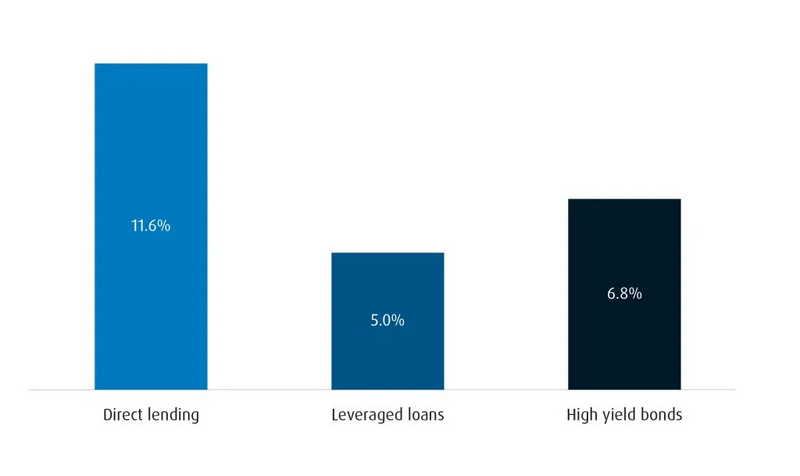

Private credit has historically offered compelling performance in relation to other segments of the fixed-income market. Since the Global Financial Crisis, when private credit’s growth began to accelerate, direct lending—the most common type of private credit—has provided elevated returns and lower volatility compared to both leveraged loans and high-yield bonds.3 An examination of performance through interest rate cycles shows consistent alpha generation over similar investments. When measured over seven different periods of restrictive monetary policy comparable to the current environment, between the first quarter of 2008 and the third quarter of 2023 direct lending yielded average returns of 11.6%, compared with 5% for leveraged loans and 6.8% for high-yield bonds, according to Morgan Stanley.

Private credit outperformance over high-rate periods (Q1 2008-Q3 2023)

Source: BMO Global Asset Management/Morgan Stanley.4

To be sure, floating rate credit will be affected by a falling interest rate environment, and investors may rightly ask about yield compression. Yet in such a scenario, it is worth noting that the underlying borrowing businesses gain additional flexibility because of lower benchmark rates, reducing financial stress and default risk.

We are also very unlikely to return to a zero-bound interest rate policy environment. Instead, rates are likely normalizing into a positive range for yields and underlying borrowers. Even under the most acute scenarios, private credit’s resilience shows. According to Goldman Sachs, during the depths of the pandemic, borrowers and lenders worked together and private credit posted a lower default rate than leveraged loans.5

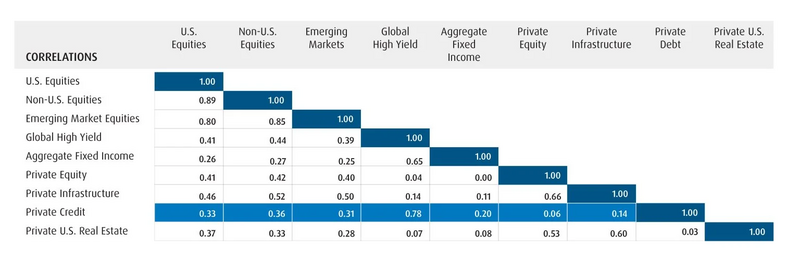

Low correlations

Private credit investments generally have low correlations to traditional equity and bond markets, providing important diversification benefits within a broader investment portfolio (see chart). This can contribute to reduced volatility and improved risk-adjusted returns.3

Source: Russell Investments, 2022.

Additionally, investors benefit from a wide range of sub-asset classes and strategies within private debt.

In general, the majority of private credit lending is in the form of floating-rate investments that change as rates change, offering real-time interest rate mitigation compared to other interest-bearing assets, like fixed-rate bonds. There are several broad categories that define the private debt market, including but not limited to, direct lending, secondary credit (mezzanine), distressed debt and special situations.

Our present areas of focus are geared towards the opportunity set within Canadian commercial real estate lending, and lending to private equity-backed companies–known as sponsor finance.

New opportunities

Commercial real estate (CRE) has historically delivered reliable risk-adjusted returns and has grown into one of the most important sleeves of institutional portfolios. Access to high-quality CRE private credit, however, remains a significant challenge for many other investors.

That is changing, as asset managers including BMO GAM seek to create new opportunities within the asset class for a wider number of investors. One potential option is the opportunity for investors to benefit from the full weight of a lender such as BMO and its risk management practices, funding a diversified range of senior debt within the Canadian CRE market. Within the current environment, effective investment management could reasonably expect to target yields in the mid/high single-digit range.7 BMO GAM expects a similarly constructed opportunity to be available likely in the fall 2024.

Similar to other private market offerings from BMO GAM, the fund structure should be structured in an open-ended evergreen format, which we believe provides access to the widest available number of Canadian accredited investors while providing certain liquidity features.

For investors, strong covenant protections and senior bondholder status should be paramount considerations.

Private equity sponsored finance represents another significant private lending opportunity, and is rooted in the very origins of the asset class more than a decade and a half ago. It represents a powerful financial strategy where a financial sponsor, often a private equity firm, invests meaningful equity in a company and a lender provides loans to that company to support its acquisition, growth, or restructuring by the sponsor. This is a common strategy in leveraged buyouts or mergers and acquisitions scenarios. The phrases “private equity backed,” “sponsor backed,” “sponsored finance,” and “sponsor finance” are commonly used interchangeably.

These lenders form funds that focus on loans to sponsor backed companies. Sponsored finance fund managers typically participate within a syndication of credit providers to capitalize or lend to a private equity sponsor company. Aside from covenant protections and senior positioning in the capital structure, a fund manager and its investors understand that private equity sponsors own equity in these businesses, and are motivated to have them perform well such that they can affect a successful exit. Effective sponsored finance fund managers also leverage expertise to deliver enhanced returns. In the present environment, investors may expect low double-digit target yields from a well-managed sponsored finance fund.

For private credit investors, strong covenant protections and senior bondholder status in capital structures that provide first-in-line access to cash and assets should be paramount considerations for any fund or strategy invested in.

Seniority in capital structure

Despite the emergence of a more favourable rate environment default rates could become less stable. Yet even then, private debt may still outperform public.5 Robust lender selection, due diligence and strong lending structures provide the tools to safeguard capital and generate alpha.

Loan covenants provide early warnings so that we, as the portfolio managers, see any default risks in advance of significant trouble, allowing us to work directly with sponsors or underlying borrowers. The relationship is often direct.

The kinds of transactions that would be sought would seek protections that provide quicker recourse, and allow us to come to the table in times of impending strain. Direct access to borrowers and financials can provide the ability to direct beneficial workout situations and maximize recovery value.

Positions that are senior in the capital structure are of the utmost importance so, if there is difficulty, the investor is at the very top of the “waterfall,” often with first claim on assets or cash. This compares favourably to junior bondholders, preferred stock, or common equity investors. The sponsor finance opportunities BMO GAM would focus on wouldn’t target non-senior credit.9

While private credit has distinct advantages, these strengths aren’t universal across the market. It is for the reasons above that fund manager and asset type selection are vital as the opportunity grows for more investors to access the asset class.

For more information

Contact your Regional BMO Global Asset Management Representative or the BMO GAM Alternatives Team at bmogamalts@bmo.com.

Insights

Sources

1“BlackRock Says Private Debt Will Double to $3.5 Trillion by 2028,” Bloomberg, October 26, 2023

2Accredited investors can include, among other things and without limitation, an individual whose net income before taxes exceeded $200,000 in each of the two most recent calendar years; whose net income before taxes combined with that of a spouse exceeded $300,000 in each of the two most recent calendar years; an individual who, either alone or with a spouse, beneficially owns financial assets having an aggregate realizable value that before taxes, but net of any related liabilities, exceeds $1,000,000; an individual who, either alone or with a spouse, has net assets of at least $5,000,000. National Instrument 45-106 – Prospectus Exemptions; Private Capital Markets Association of Canada.

3Understanding Private Credit, Ashwin Krishnan, Co-Head of North America Private Credit. Morgan Stanley Investment Management, June 20, 2024.

4Data represents the period from March 30, 2008 to September 30, 2023. Calculated as annualized average returns divided by volatility. Volatility is measured using standard deviation. Direct Lending is represented by the Cliffwater Direct Lending Index (CDLI) and is calculated from quarterly data, which has been annualized. High Yield Bonds is represented by the ICE BofA High Yield Index calculated from annualized monthly data. Leveraged Loans is represented by the Morningstar LSTA US Leveraged Loan Index calculated from annualized monthly data.

5Private credit may outperform public bonds as defaults rise, Stephanie Rader, Global Head of Private Credit Client Solutions, and James Gelfer, in Portfolio Solutions for Alternatives Capital Markets and Strategy. Goldman Sachs Asset Management, May 11, 2023.

3Understanding Private Credit, Ashwin Krishnan, Co-Head of North America Private Credit. Morgan Stanley Investment Management, June 20, 2024.

7There is no guarantee with respect to the performance of a private credit product.

5Private credit may outperform public bonds as defaults rise, Stephanie Rader, Global Head of Private Credit Client Solutions, and James Gelfer, in Portfolio Solutions for Alternatives Capital Markets and Strategy. Goldman Sachs Asset Management, May 11, 2023.

9Certain other private credit products could contain different features.

Disclaimers

For Advisors and Institutional Client Use Only

“BMO (M-bar roundel symbol)” is a registered trademark of Bank of Montreal, used under licence.

BMO Global Asset Management (BMO GAM) is a brand name under which BMO Asset Management Inc. and BMO Investments Inc. operate. Certain of the products and services offered under the brand name, BMO Global Asset Management, are designed specifically for various categories of investors in Canada and may not be available to all investors. Products and services are only offered to investors in Canada in accordance with applicable laws and regulatory requirements.

The information contained herein: (1) is confidential and proprietary to BMO GAM; (2) may not be reproduced or distributed without the prior written consent of BMO GAM; and (3) has been obtained from third-party sources believed to be reliable but which have not been independently verified. BMO GAM and its affiliates do not accept any responsibility for any loss or damage that results from the use of this information. This article has been prepared solely for information purposes by BMO GAM.

The information provided herein does not constitute a solicitation of an offer to buy, or an offer to sell securities nor should the information be relied upon as investment advice. Past performance is no guarantee of future results.

Certain statements included in this material constitute forward-looking statements, including, but not limited to, those identified by the expressions “expect”, “intend”, “will” and similar expressions. The forward-looking statements are not historical facts but reflect BMO GAM’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. Although BMO GAM believes that the assumptions inherent in the forward-looking statements are reasonable, forward-looking statements are not guarantees of future performance and, accordingly, readers are cautioned not to place undue reliance on such statements due to the inherent uncertainty therein. BMO GAM undertakes no obligation to update publicly or otherwise revise any forward-looking statement or information whether as a result of new information, future events or other such factors which affect this information, except as required by law.